Experiencing financial hardship can significantly impact your credit score, making it challenging to secure loans, rent an apartment, or even get a job. Rebuilding credit after facing job loss, medical emergencies, or other unexpected events can seem daunting, but it’s absolutely achievable with a strategic approach. This article will provide a comprehensive guide on how to rebuild credit after financial hardship, offering practical steps to improve your credit report and regain financial stability. We’ll cover key strategies, including budgeting, debt management, and leveraging credit-building tools, to help you navigate the path to credit repair and a brighter financial future.

If you’re struggling with bad credit due to financial hardship, you’re not alone. Millions of people face credit challenges, and understanding how to effectively address them is crucial. Whether you’re dealing with collection accounts, late payments, or even bankruptcy, this guide will equip you with the knowledge and resources to rebuild your credit score. We’ll explore the impact of financial hardship on your credit and provide actionable advice for credit improvement, helping you move forward with confidence and reclaim your financial well-being.

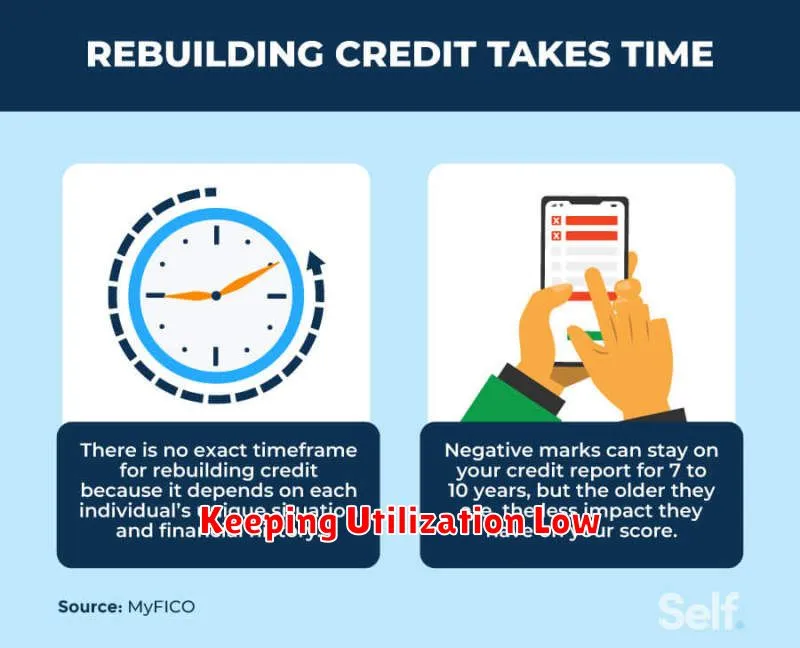

Signs Your Credit Needs Repair

Several key indicators can point to the need for credit repair. One major sign is consistent denial of credit applications. Whether it’s a credit card, loan, or even a rental application, repeated rejections strongly suggest underlying credit issues. Another significant warning sign is receiving unusually high interest rates on approved credit. Lenders often offer less favorable terms to individuals with poor credit history. Finally, consistently low credit scores across different reporting agencies are a clear indicator of a need for repair. Regularly checking your credit reports can help you identify these potential problems early on.

Beyond denials and high interest rates, there are more subtle signs to watch for. Unexpected collection notices for debts you believe are paid or don’t recognize can be a red flag. Similarly, errors on your credit reports, such as incorrect personal information or accounts you don’t recognize, require immediate attention and correction. These inaccuracies can negatively impact your creditworthiness. Additionally, if you find yourself maxing out your credit cards or struggling to make minimum payments, it’s a strong indication of potential credit difficulties that may worsen without intervention.

Taking proactive steps to address these issues is crucial. Begin by obtaining copies of your credit reports from all three major credit bureaus. Carefully review them for errors and inconsistencies. If you identify any inaccuracies, dispute them directly with the bureaus and the creditors involved. Developing a realistic budget and payment plan can also help you manage your existing debt and prevent further damage to your credit. Consider seeking guidance from a reputable credit counseling agency if you feel overwhelmed or unsure about how to proceed. Addressing these issues head-on is essential for building a stronger financial future.

Understanding Credit Report Errors

Credit report errors can significantly impact your financial health, affecting your ability to secure loans, rent an apartment, or even obtain employment. These inaccuracies can range from simple clerical mistakes, like an incorrect address or phone number, to more serious issues such as accounts that don’t belong to you or inaccurate payment histories. It’s crucial to regularly review your credit reports from all three major credit bureaus (Equifax, Experian, and TransUnion) to identify and address any discrepancies.

Common types of errors include inaccurate personal information, incorrect account balances, accounts belonging to someone else, duplicate accounts, and incorrect payment history. Identifying these errors requires careful scrutiny of each item listed on your report. Compare the information to your own records, such as bank statements and billing statements, to pinpoint any inconsistencies.

If you find an error, you must dispute it with the respective credit bureau. This typically involves submitting a written dispute along with supporting documentation. The bureau is then obligated to investigate the claim and correct any verified inaccuracies. Regular monitoring and prompt action are essential to maintaining the accuracy of your credit reports and protecting your financial well-being.

Secured Credit Cards as a Starting Point

For individuals with limited or damaged credit history, secured credit cards offer a viable path towards building or rebuilding creditworthiness. Unlike traditional credit cards, secured cards require a cash deposit that typically serves as the credit limit. This deposit minimizes the risk for the issuer, allowing them to approve applicants who might otherwise be denied. By responsibly using a secured card and making timely payments, cardholders demonstrate positive credit behavior, which is reported to the major credit bureaus. This positive reporting helps establish a credit history or repair a damaged one, paving the way for future access to traditional credit products.

The key advantage of secured credit cards lies in their accessibility. They are specifically designed for individuals who may face challenges obtaining unsecured credit. This includes people who are new to credit, have a history of late payments, or have declared bankruptcy. While the deposit requirement may seem like a hurdle, it ultimately serves as a valuable tool for learning responsible credit management. The card’s spending limit, tied to the deposit, encourages mindful spending habits and helps prevent accumulating excessive debt.

Choosing the right secured credit card involves considering several factors. Fees, including annual fees, application fees, and late payment fees, should be compared across different offers. Additionally, the card’s APR (Annual Percentage Rate) is important, although it becomes less relevant with consistent on-time payments. Finally, it’s crucial to ensure the card reports to all three major credit bureaus (Experian, Equifax, and TransUnion), maximizing the impact on your credit score.

Keeping Utilization Low

Maintaining low credit utilization is crucial for a healthy credit score. Credit utilization refers to the percentage of your available credit that you are currently using. Keeping this percentage low demonstrates responsible credit management and suggests to lenders that you are not overextending yourself financially. A good rule of thumb is to keep your utilization below 30%, with 10% or lower being ideal for maximizing your credit score.

High utilization can negatively impact your credit score in several ways. It can signal to lenders that you are heavily reliant on credit, potentially increasing the risk of late payments or default. Additionally, high utilization can make it more difficult to obtain new credit, as lenders may view you as a higher-risk borrower. Consistently monitoring and managing your credit utilization is a key component of building and maintaining good credit.

Several strategies can help you keep your utilization low. These include paying down balances strategically, increasing credit limits (responsibly), and spreading spending across multiple cards. By actively managing your credit utilization, you can positively influence your credit score and improve your overall financial health.

Paying On Time Every Month

Paying your bills on time every month is crucial for maintaining a good credit score. Late payments can negatively impact your credit report, making it harder to obtain loans, rent an apartment, or even secure certain jobs. Establishing a consistent pattern of on-time payments demonstrates financial responsibility to lenders and creditors.

There are several strategies to help ensure timely payments. Setting up automatic payments through your bank or credit card company is a convenient option. Alternatively, creating calendar reminders or using budgeting apps can provide timely alerts. Prioritize paying essential bills like rent/mortgage and utilities first, then allocate funds towards other debts.

If you anticipate difficulty making a payment, communicate with your creditor proactively. They may offer options such as a payment plan or due date extension to help avoid late fees and negative credit reporting. Ignoring the problem will only worsen the situation, so reaching out is always the best course of action.

Avoiding New Debt While Rebuilding

Rebuilding your finances after accumulating debt can be challenging, and the key to success lies in avoiding new debt. This requires a budget that tracks income and expenses, allowing you to identify areas where you can cut back. Prioritize paying down existing debt using strategies like the debt snowball or avalanche method. It’s crucial to resist the temptation of new credit offers and focus on building an emergency fund. This safety net will help cover unexpected expenses, preventing you from relying on credit cards and falling back into debt.

Changing spending habits is essential. Differentiate between needs and wants, and find ways to reduce spending on non-essential items. Consider preparing meals at home more often, exploring free or low-cost entertainment options, and avoiding impulsive purchases. Seek out community resources that can provide support and assistance, such as credit counseling services or financial literacy programs. These resources can offer valuable guidance and strategies for managing your finances effectively.

Building a long-term financial plan is crucial for sustained success. This includes setting financial goals, such as saving for retirement or a down payment on a house. Explore opportunities to increase your income, such as taking on a part-time job or developing new skills. Continuously monitor your progress and adjust your budget as needed. By adopting a proactive and disciplined approach to managing your finances, you can avoid new debt and build a secure financial future.

Monitoring Your Progress

Monitoring your progress is crucial for achieving your goals. Regularly tracking your advancements helps you stay motivated, identify potential roadblocks, and adjust your strategies as needed. Whether you’re working towards a personal or professional objective, taking the time to assess your progress allows you to celebrate successes and learn from setbacks.

There are various methods you can use to monitor progress. You can create checklists, use spreadsheets, or utilize project management software. The key is to choose a method that works best for you and the specific goal you’re tracking. Be sure to set realistic milestones and track your progress consistently.

By consistently monitoring your progress, you gain valuable insights into your performance. This allows you to make informed decisions and stay focused on achieving the desired outcome. Remember to be flexible and adjust your approach as necessary. Consistent monitoring empowers you to stay on track and reach your full potential.

Staying Consistent Over Time

Consistency is key to achieving long-term goals. Whether you’re aiming to improve your fitness, learn a new skill, or build a successful business, showing up consistently, even in small ways, builds momentum and creates lasting change. It’s not about perfect execution every time, but rather about making the effort and sticking with it, even when motivation wanes.

Creating a routine can greatly aid in staying consistent. Set a schedule for your chosen activity and treat it like an important appointment. Break down larger goals into smaller, manageable steps to avoid feeling overwhelmed. Tracking your progress can also be beneficial, as seeing how far you’ve come is a powerful motivator. Remember to celebrate small wins along the way to maintain enthusiasm.

Finally, be kind to yourself. There will be days when you miss a workout, skip a practice session, or fall short of your expectations. Don’t let these setbacks derail your overall progress. Acknowledge them, learn from them, and get back on track as soon as possible. Consistency is about the big picture, not individual slip-ups. Focus on the overall trend and keep moving forward.

{kind=link}